Investments

Complete Real Estate Investment Guide 2026: Everything You Need to Know About Property Investment in India

16 Dec 2025

Investments

16 Dec 2025

Content

No Blogs content found

It looks like there haven’t been any blogs yet!

Real estate investment in India has transformed from a simple shelter purchase into a sophisticated wealth creation strategy. Over the past two decades, property investment has emerged as one of the most preferred asset classes for Indian households, competing with gold, fixed deposits, and equity markets for investor attention and capital allocation.

Real estate investment means purchasing property with the primary goal of generating returns through rental income, capital appreciation, or both. Unlike buying a home for personal use, investment properties are acquired specifically to build wealth over time.

The fundamental difference between real estate investment and other asset classes lies in its physical nature. A property stands on actual land, has walls and a roof, and serves a real purpose beyond just being a financial instrument. This tangible presence provides psychological comfort that paper assets like stocks or bonds cannot match.

Real estate investment can take multiple forms including residential apartments, commercial office spaces, retail shops, industrial warehouses, agricultural land, or even fractional ownership through Real Estate Investment Trusts. Each category offers different risk profiles, return characteristics, and capital requirements.

The year 2026 presents specific opportunities and conditions that make real estate investment particularly relevant for Indian investors. Several macroeconomic and demographic factors are converging to create a favorable environment for property investment.

India's urban population is growing by approximately 10 million people annually. The 2021 census data shows that 35 percent of Indians now live in urban areas, up from 28 percent in 2001. This migration from rural to urban centers creates sustained demand for housing in cities.

Every person moving to a city needs a place to live, whether as a renter or eventual homeowner. This demographic shift provides a fundamental demand driver that supports property values and rental markets. Cities like Bangalore, Hyderabad, and Pune are absorbing 200,000 to 300,000 new residents each year, creating immediate housing demand.

The government's infrastructure push through programs like Bharatmala for highways, dedicated freight corridors for railways, and metro expansions in tier 1 and tier 2 cities is opening up new areas for residential and commercial development.

Properties located along these infrastructure corridors typically see significant appreciation as connectivity improves and travel times reduce. The 2026 timeframe coincides with the completion of several major infrastructure projects that will unlock value in previously underserved locations.

Home loan interest rates in early 2025 range from 8.5 to 9.5 percent, which remains reasonable from a historical perspective. While rates have increased from the pandemic era lows of 6.5 to 7 percent, they are still below the 10 to 12 percent levels common in the 2010 to 2014 period.

These moderate rates make leveraged property investment viable, as rental yields and appreciation can exceed borrowing costs. A property appreciating at 8 percent annually with rental yield of 3 percent generates 11 percent total returns, comfortably exceeding the 9 percent borrowing cost.

The implementation of RERA in 2016 has gradually improved transparency and accountability in the real estate sector. Buyers now have better legal protection, clearer project timelines, and recourse against developer defaults.

This regulatory improvement reduces some of the risks that historically plagued Indian real estate investment, making it more attractive to cautious investors.

The income tax benefits available on home loans continue to provide significant advantages for property investors.

| Infrastructure Project | Completion Timeline | Impact on Real Estate |

|---|---|---|

| Delhi–Mumbai Expressway | 2024–2025 | Opens Gurgaon and Sohna corridor |

| Bangalore Metro Phase 3 | 2026–2027 | Unlocks peripheral areas |

| Pune Metro | 2025–2026 | Connects Hinjewadi to city center |

| Jewar Airport (Noida) | 2024–2025 |

| Tax Benefit | Section | Maximum Deduction | Applicable To |

|---|---|---|---|

| Principal Repayment | 80C | ₹1.5 lakhs per year | All home loans |

| Interest Payment (Self Occupied) | 24(b) | ₹2 lakhs per year | Owner occupied property |

| Interest Payment (Let Out) | 24(b) | Unlimited | Rental properties |

| First Time Buyer Additional | 80EEA | ₹1.5 lakhs per year | First home under ₹45 lakhs |

These tax benefits improve net returns and make real estate competitive with other investment options on an after tax basis. For someone in the 30 percent tax bracket, the maximum deductions can save up to 1.5 lakhs in taxes annually.

Real estate investment in India encompasses several distinct categories, each with different risk profiles, return characteristics, and capital requirements.

Residential properties include apartments, independent houses, villas, and plotted developments intended for people to live in. This category represents the largest segment of real estate investment in India, accounting for approximately 70 percent of total real estate investment by value.

The returns from residential property come from two sources. Rental income provides regular cash flow, with gross rental yields in major Indian cities ranging from 2 to 4 percent annually. Capital appreciation provides the larger component of returns, with property values in well located areas appreciating 6 to 12 percent annually over long periods.

| City | Average Annual Appreciation | Rental Yield | Total Return |

|---|---|---|---|

| Bangalore | 8–10% | 2.5–3.5% | 10.5–13.5% |

| Hyderabad | 9–12% | 3–4% | 12–16% |

| Pune | 7–9% | 2.5–3% | 9.5–12% |

| Gurgaon | 6–8% | 2–3% | 8–11% |

| Mumbai | 4–6% | 2–2.5% | 6–8.5% |

| Noida | 5–7% | 2.5–3.5% | 7.5–10.5% |

Commercial properties include office spaces, retail shops, showrooms, and business centers leased to companies and businesses. This category typically requires higher capital investment compared to residential properties but offers better rental yields.

Commercial property rental yields in prime locations range from 6 to 9 percent annually, significantly higher than residential yields. Lease agreements for commercial properties typically run for 3 to 9 years with built in rent escalation clauses of 5 to 15 percent every few years.

| Factor | Residential | Commercial |

|---|---|---|

| Entry Capital | ₹30–50 lakhs | ₹50 lakhs – ₹2 crores |

| Rental Yield | 2–4% | 6–9% |

| Lease Duration | 11 months | 3–9 years |

| Rent Escalation | 5–10% annually | 10–15% every 3 years |

| Liquidity | High | Moderate to Low |

| Maintenance | Owner responsibility | Often tenant responsibility |

| Economic Sensitivity | Low | High |

The challenges with commercial property include higher capital requirements, with entry level commercial investments starting around 50 lakhs to 1 crore in most cities. The market is less liquid than residential, with fewer potential buyers and longer transaction times. Commercial property values and rental demand are more sensitive to economic cycles, with vacancies increasing during recessions.

REITs provide a way to invest in real estate without directly owning physical property. These are companies that own and operate income generating real estate, and they are required to distribute at least 90 percent of their taxable income to shareholders as dividends.

Indian REITs launched in 2019, with Embassy Office Parks REIT and Mindspace Business Parks REIT being the first to list. These REITs own portfolios of commercial office buildings leased to multinational corporations and Indian companies.

| REIT Name | Listing Year | Portfolio Value | Dividend Yield | Minimum Investment |

|---|---|---|---|---|

| Embassy Office Parks REIT | 2019 | ₹30,000+ crores | 6.5–7.5% | ₹50,000 – ₹1 lakh |

| Mindspace Business Park REIT | 2020 | ₹20,000+ crores | 6–7% | ₹50,000 – ₹1 lakh |

| Brookfield India REIT | 2021 | ₹25,000+ crores | 6.5–7% | ₹50,000 – ₹1 lakh |

The returns from REITs come from dividend income, which typically yields 6 to 8 percent annually, and potential capital appreciation of the REIT units themselves. The dividend income is taxable in the hands of investors, unlike the tax benefits available on direct property ownership.

Land investment involves purchasing plots without any construction, either in urban areas approved for development or in agricultural zones. This category requires the longest investment horizon and carries specific risks related to land use regulations and development approvals.

Urban land investment works best in areas where infrastructure development is planned or underway. Plots located along upcoming metro corridors, highway expansions, or near proposed IT parks and industrial zones can appreciate significantly as development progresses.

Agricultural land investment is restricted by law in most states, with only farmers or agricultural companies allowed to purchase agricultural land. Some investors circumvent these restrictions through various means, but this creates legal risks that can result in property seizure or criminal prosecution.

Understanding the current real estate market conditions and future trends is essential for making informed investment decisions. The Indian property market in 2026 presents a mixed picture with strong fundamentals in some segments and cities while others face challenges.

The Indian real estate market has recovered from the pandemic induced slowdown of 2020 and 2021, with residential sales volumes in 2024 reaching pre pandemic levels in most major cities. The market is characterized by consolidation, with established developers gaining market share while smaller, financially weaker developers exit or get acquired.

| Metric | Value | Change from 2023 |

|---|---|---|

| Total Housing Units Sold | 4.2 lakh units | +12% |

| Average Price Appreciation | 7.5% | +2% |

| Unsold Inventory | 6.8 lakh units | −8% |

| New Project Launches | 3.9 lakh units | +15% |

| Under Construction Projects | 12.5 lakh units | +5% |

The residential segment dominates transaction volumes, accounting for 75 percent of total real estate activity by number of transactions. The affordable and mid segment housing categories (properties priced between 30 lakhs and 1 crore) represent the largest share of sales, driven by end user demand from first time homebuyers and nuclear families.

The commercial real estate segment has shown strong recovery, particularly in office spaces driven by IT and business services companies expanding their operations. The return to office trend after the pandemic has increased demand for quality office spaces in prime locations.

Retail real estate faced challenges during the pandemic but is recovering gradually as consumer spending normalizes. Malls and high street retail in prime locations are performing well, while secondary locations continue to struggle with vacancies.

The real estate sector is witnessing consolidation, with the top 10 developers accounting for an increasing share of new launches and sales. This consolidation benefits buyers by reducing the risk of dealing with financially weak developers who may delay projects or default.

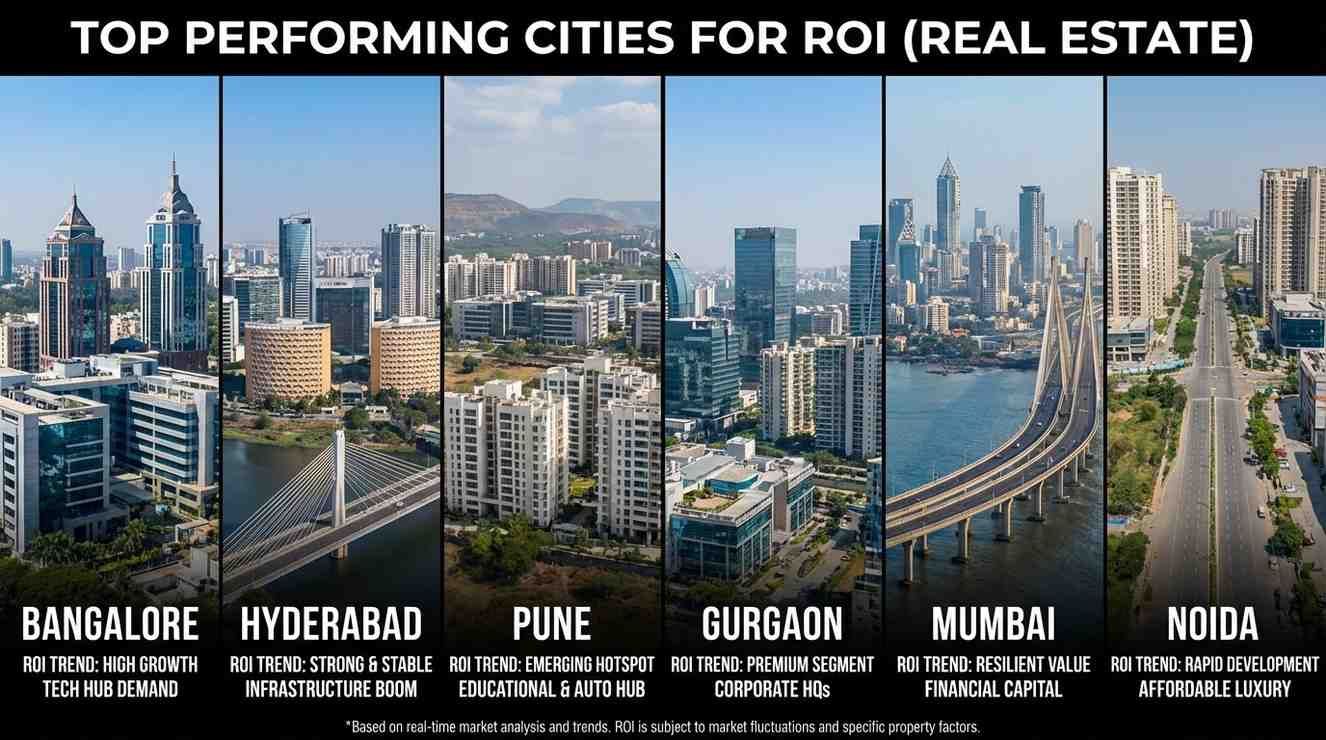

Different cities offer varying return profiles based on local economic conditions, job creation, infrastructure development, and supply demand dynamics. Understanding which cities are performing well helps investors allocate capital to locations with the best risk adjusted returns.

Bangalore continues to lead in terms of total returns combining rental yield and capital appreciation. The city's position as India's technology capital drives consistent demand from IT professionals and companies.

The best performing micro markets in Bangalore include Whitefield, Electronic City, Sarjapur Road, and areas along the upcoming metro corridors. Properties in these locations have appreciated 40 to 60 percent over the past five years.

Hyderabad has emerged as a strong performer, offering better appreciation than most other metros while maintaining reasonable entry prices. The city's growth is driven by IT sector expansion, pharmaceutical industry presence, and proactive government policies.

The HITEC City, Gachibowli, Kondapur, and Kokapet areas have shown exceptional appreciation, with properties doubling in value over the past six to seven years. The upcoming airport expansion and pharma city development will create new growth corridors.

Pune offers a balanced market with steady appreciation, reasonable rental yields, and diverse economic drivers including IT, manufacturing, and education sectors.

The Hinjewadi IT corridor, Baner, Wakad, and areas along the metro route offer good investment potential. The upcoming Pune Ring Road will open new areas for development and appreciation.

Gurgaon (Gurugram) serves as the primary satellite city for Delhi, hosting numerous multinational corporations and offering modern infrastructure. The market has matured, with appreciation rates moderating but remaining positive.

The Golf Course Extension Road, Sohna Road, Southern Peripheral Road, and Dwarka Expressway corridor offer investment opportunities at different price points. The upcoming infrastructure projects will support continued appreciation.

Mumbai remains India's financial capital but offers lower appreciation rates due to already high property prices and limited land availability. The market is characterized by stability rather than explosive growth.

The western suburbs including Andheri, Goregaon, and Malad offer better value than South Mumbai. The Thane and Navi Mumbai markets provide more affordable entry points with decent appreciation potential.

The Noida region offers affordable entry prices and benefits from proximity to Delhi and the upcoming Jewar Airport. The market has been volatile historically but is stabilizing under RERA regulations.

The Noida Expressway, Greater Noida West, and areas near the upcoming Jewar Airport offer investment potential. Buyers should focus on projects from established developers with RERA registration and clear delivery timelines.

| City | Best For | Entry Price (2 BHK) | 5 Year Appreciation Potential |

|---|---|---|---|

| Bangalore | High growth, tech jobs | ₹60–80 lakhs | 50–70% |

| Hyderabad | Best ROI, affordable | ₹45–65 lakhs | 55–75% |

| Pune | Balanced returns | ₹50–70 lakhs | 40–55% |

| Gurgaon | Stable rental income | ₹70–90 lakhs | 35–50% |

| Mumbai | Capital preservation | ₹1.2–1.8 crore | 25–35% |

| Noida | Affordable entry | ₹40–60 lakhs | 30–45% |

Beyond the established metros, several tier 2 cities and emerging localities within metros offer attractive investment opportunities with higher growth potential and lower entry barriers.

Ahmedabad has emerged as a strong real estate market driven by the city's position as Gujarat's commercial capital, the presence of manufacturing industries, and the development of the GIFT City financial hub.

Properties in areas like Bopal, Shela, and South Bopal have appreciated 50 to 70 percent over the past five years. The upcoming metro expansion and the Ahmedabad Mumbai bullet train project will further boost property values.

The Chandigarh tricity region offers a planned urban environment with good infrastructure and quality of life. The IT sector growth in Mohali and the presence of educational institutions create rental demand.

Investment opportunities exist in Mohali, Zirakpur, and New Chandigarh at price points 40 to 50 percent lower than Delhi NCR for comparable properties.

Indore has shown consistent growth driven by its position as Madhya Pradesh's commercial center, good connectivity, and relatively affordable property prices.

The city offers entry prices of 30 to 50 lakhs for 2 BHK apartments with appreciation potential of 8 to 10 percent annually. The upcoming metro project will create new investment corridors.

Jaipur combines tourism, education, and emerging IT sectors to create diverse economic drivers. The metro connectivity and infrastructure improvements are opening new areas for development.

Properties in areas like Jagatpura, Malviya Nagar, and Vaishali Nagar offer investment potential with entry prices significantly lower than metros.

Within established metros, certain localities are emerging as high growth areas due to infrastructure development or changing usage patterns.

Understanding price trends and making reasonable predictions helps investors time their entry and exit decisions. While real estate markets are difficult to predict with precision, certain trends and drivers provide directional guidance.

The Indian residential real estate market is expected to see moderate appreciation of 6 to 9 percent annually over the 2026 to 2027 period. This represents a normalization from the higher appreciation rates of 2022 to 2024 when pent up pandemic demand drove prices higher.

| Segment | 2026 Outlook | 2027 Outlook | Key Drivers |

|---|---|---|---|

| Affordable Housing | 5–7% growth | 6–8% growth | Government schemes, first-time buyers |

| Mid Segment | 6–8% growth | 7–9% growth | End-user demand, upgraders |

| Premium | 7–10% growth | 8–11% growth | Limited supply, wealth creation |

| Luxury | 8–12% growth | 9–13% growth | Ultra HNI demand, scarcity value |

Bangalore and Hyderabad are expected to continue outperforming other metros with appreciation of 8 to 12 percent annually, driven by strong job creation and infrastructure development. Pune should deliver steady 7 to 9 percent appreciation supported by metro completion and diverse economic base.

Gurgaon and Noida will likely see moderate 6 to 8 percent appreciation as markets mature and supply catches up with demand. Mumbai may continue with lower 4 to 6 percent appreciation due to already high base prices and limited land availability.

Rental rates are expected to grow 5 to 8 percent annually across major cities, driven by continued migration to urban centers and preference for renting among young professionals. This rental growth will gradually improve rental yields from current levels of 2 to 4 percent to 2.5 to 4.5 percent by 2027.

The gap between property price appreciation and rental growth is expected to narrow, making rental yields more attractive for investors focused on income generation rather than pure capital appreciation.

Successful real estate investment requires a clear strategy aligned with your financial goals, risk tolerance, and investment horizon. Different strategies suit different investor profiles and market conditions.

The buy and hold strategy involves purchasing property and retaining ownership for an extended period, typically 5 to 15 years or longer. This approach focuses on long term capital appreciation and steady rental income rather than quick profits.

You identify a property in a location with strong fundamentals including job growth, infrastructure development, and limited supply. You purchase the property using a combination of own funds and home loan. You rent out the property to generate income that covers part or all of the EMI. You hold the property through market cycles, benefiting from long term appreciation.

Consider a 2 BHK apartment in Bangalore purchased for 60 lakhs in 2026. You make a down payment of 12 lakhs and take a home loan of 48 lakhs at 9 percent interest for 20 years. Your monthly EMI is approximately 43,200 rupees.

You rent the property for 25,000 rupees per month initially. The rental income covers 58 percent of your EMI, with you contributing 18,200 rupees monthly from your pocket. You claim tax deductions on the home loan, saving approximately 8,000 rupees monthly in taxes, reducing your net outflow to 10,200 rupees monthly.

Over 10 years, assuming 8 percent annual appreciation, the property value grows to approximately 1.29 crores. Your loan balance after 10 years is approximately 32 lakhs. Your equity in the property is 97 lakhs (property value minus loan balance).

Your total investment over 10 years includes the initial 12 lakh down payment plus 10,200 rupees monthly for 120 months, totaling approximately 24.24 lakhs. Your equity of 97 lakhs against investment of 24.24 lakhs represents a 300 percent return over 10 years, or approximately 15 percent annualized return.

The fix and flip strategy involves purchasing properties that need renovation or are available at below market prices, improving them, and selling quickly for profit. This approach requires more active involvement and carries higher risks compared to buy and hold.

You identify properties available at discounts due to distress sales, legal issues resolved, or poor condition. You purchase the property at below market rates. You invest in renovations, repairs, or legal clearances to enhance value. You sell the property within 6 to 24 months at market rates, capturing the difference as profit.

You purchase a 2 BHK apartment in a 10 year old building for 50 lakhs, which is 15 percent below the market rate of 59 lakhs for similar apartments in good condition. The property needs renovation including new flooring, painting, kitchen and bathroom updates.

You invest 5 lakhs in renovation over 3 months. Your total investment is 55 lakhs plus transaction costs of approximately 2 lakhs, totaling 57 lakhs. You sell the renovated property for 62 lakhs after 6 months.

Your gross profit is 5 lakhs (62 lakhs sale price minus 57 lakhs total investment). You pay short term capital gains tax of approximately 1.5 lakhs (30 percent of profit). Your net profit is 3.5 lakhs on an investment of 57 lakhs over 9 months, representing approximately 6 percent return in 9 months or 8 percent annualized.

The rental income strategy focuses on generating regular cash flow from properties rather than primarily seeking capital appreciation. This approach suits investors looking for passive income to supplement salary or retirement income.

Rental yield measures the annual rental income as a percentage of property value. Gross rental yield is calculated as annual rent divided by property value. Net rental yield deducts expenses like maintenance, property tax, and vacancy periods.

| City | Residential Yield | Commercial Yield | Best Rental Areas |

|---|---|---|---|

| Bangalore | 2.5–3.5% | 7–9% | Whitefield, Electronic City |

| Hyderabad | 3–4% | 7–9% | HITEC City, Gachibowli |

| Pune | 2.5–3% | 6–8% | Hinjewadi, Kharadi |

| Gurgaon | 2–3% | 6–8% | Cyber City vicinity |

| Mumbai | 2–2.5% | 6–7% | Andheri, Powai |

| Noida | 2.5–3.5% | 6–8% | Sector 62, Sector 78 |

You purchase a 2 BHK apartment near an IT park for 70 lakhs. You make a down payment of 14 lakhs and take a loan of 56 lakhs at 9 percent for 20 years. Your monthly EMI is 50,400 rupees.

You furnish the property with basic furniture and appliances for 3 lakhs. You rent it for 32,000 rupees per month. Your rental income covers 63 percent of the EMI, with you contributing 18,400 rupees monthly.

After tax deductions on the home loan, your net monthly outflow is approximately 8,000 rupees. Over time, as you pay down the loan and rents increase, your cash flow improves. By year 10, with rents growing at 6 percent annually, your rental income is approximately 57,000 rupees while your EMI remains 50,400 rupees, creating positive cash flow of 6,600 rupees monthly.

Group buying involves multiple investors pooling resources to purchase properties, typically negotiating better prices and terms from builders due to bulk buying power. This strategy has gained popularity through platforms like TogetherBuying that facilitate collective property investment.

A platform or organizer identifies a property project and negotiates with the builder for bulk purchase discounts. Multiple investors join the group, each committing to purchase one or more units. The group collectively negotiates better prices, additional amenities, or favorable payment terms. Each investor completes their individual purchase with the negotiated benefits.

TogetherBuying has emerged as a leading platform for group property buying in India, offering several advantages to investors:

A group of 15 investors uses TogetherBuying to purchase apartments in a Gurgaon project. The builder's listed price for 2 BHK apartments is 85 lakhs. Through group negotiation, the price is reduced to 78 lakhs, a discount of 7 lakhs or 8.2 percent.

Additionally, the group negotiates free car parking worth 2.5 lakhs and club membership worth 2 lakhs, adding 4.5 lakhs in value. The total benefit is 11.5 lakhs or 13.5 percent of the original price.

Each investor saves on brokerage (typically 1.7 lakhs on an 85 lakh property), bringing total savings to approximately 13.2 lakhs per investor. This immediate value creation enhances the investment return before considering appreciation and rental income.

Investors must choose between investing in physical properties or Real Estate Investment Trusts based on their capital availability, involvement preference, and return expectations.

| Factor | Physical Property | REITs |

|---|---|---|

| Minimum Investment | ₹30–50 lakhs | ₹50,000 – ₹1 lakh |

| Liquidity | Low (months to sell) | High (instant on exchange) |

| Leverage | Yes (up to 80% home loan) | No |

| Tax Benefits | Yes (80C, 24(b)) | No |

| Management | Self-managed | Professional |

| Diversification | Single property | Multiple properties |

| Income | Rental income (monthly) | Dividend income (quarterly) |

| Returns | 8–15% total | 6–10% total |

Choose physical property if you have sufficient capital for down payment, want to use leverage to amplify returns, prefer direct control over your investment, plan to hold for 7 to 10 years or longer, and want tax benefits on home loans.

Choose REITs if you have limited capital to invest, want liquidity and ability to exit quickly, prefer passive investment without management hassles, want diversification across multiple properties, and are comfortable with market volatility.

Many investors use a combination approach, owning one or two physical properties for long term wealth creation and tax benefits while also investing in REITs for liquidity and diversification.

Proper financial planning is essential for successful real estate investment. Understanding your budget, financing options, tax implications, and return calculations helps you make informed decisions and avoid financial stress.

Determining how much you can afford to invest in real estate requires honest assessment of your financial situation, including income, expenses, existing obligations, and future needs.

Calculate your total monthly household income from all sources including salary, business income, rental income from existing properties, and investment returns. Use conservative estimates, particularly for variable income sources.

For salaried individuals, use your in hand salary after all deductions. For business owners, use average monthly income over the past 12 to 24 months, excluding exceptional one time gains.

List all monthly expenses including rent (if currently renting), utilities, groceries, transportation, insurance premiums, children's education, entertainment, and miscellaneous costs. Include annual expenses like vacations and festivals by dividing by 12.

Be realistic about expenses. Many people underestimate actual spending, leading to financial stress when EMI obligations begin.

Account for existing loans including personal loans, car loans, credit card debt, and other EMIs. Lenders consider these obligations when calculating your loan eligibility.

The general rule suggests that your total EMI obligations should not exceed 40 to 50 percent of your monthly income. This leaves an adequate buffer for other expenses and emergencies.

Monthly household income: 2 lakhs Existing EMIs: 20,000 rupees Maximum recommended total EMI: 1 lakh (50 percent of income) Available for property EMI: 80,000 rupees

With 80,000 rupees available for EMI, you can afford a home loan of approximately 72 lakhs at 9 percent interest for 20 years. With a 20 percent down payment, you can purchase a property worth approximately 90 lakhs.

Most banks require 20 percent down payment for home loans, meaning you need to arrange 20 percent of the property value from your own funds. For a 90 lakh property, you need 18 lakhs as down payment.

Additionally, you need funds for registration, stamp duty, and other transaction costs, typically 7 to 10 percent of property value. For a 90 lakh property, budget an additional 6 to 9 lakhs for these costs.

Total upfront capital required: 24 to 27 lakhs for a 90 lakh property.

Avoid taking personal loans for down payment, as this creates additional EMI burden and reduces your home loan eligibility.

Home loans make property investment accessible by allowing you to leverage your capital. Understanding loan options, eligibility criteria, and terms helps you secure favorable financing.

| Loan Type | Purpose | Interest Rate | Loan Amount |

|---|---|---|---|

| Home Purchase Loan | Buying ready or under-construction property | 8.5–9.5% | Up to 80% of property value |

| Plot Loan | Purchasing land | 9–10% | Up to 70% of land value |

| Construction Loan | Building on owned land | 9–10% | Based on construction cost |

| Home Improvement Loan | Renovation of existing property | 9.5–11% | Up to 80% of renovation cost |

| Balance Transfer | Refinancing existing home loan | 8.5–9.5% | Outstanding loan balance |

Lenders evaluate multiple factors when determining your loan eligibility and the amount they will sanction.

Your monthly income determines the EMI you can afford. Lenders typically allow EMI up to 50 to 60 percent of your gross monthly income, though 40 to 50 percent is more prudent.

Younger borrowers get longer loan tenures, while older borrowers face restrictions. Most banks offer loans up to age 60 for salary and 65 for self-employed, meaning a 45 year old can get a maximum 15 to 20 year tenure.

A CIBIL score of 750 or above is considered good and qualifies for best interest rates. Scores between 650 and 750 may get loans at higher rates. Scores below 650 face difficulty getting approval.

Your existing EMIs reduce the loan amount you qualify for. Lenders calculate your Fixed Obligation to Income Ratio (FOIR), ensuring total EMIs don't exceed 50 to 60 percent of income.

Salaried individuals need minimum 2 to 3 years work experience with at least 1 year in current organization. Self employed need a minimum 3 to 5 years in current business.

The property being purchased serves as collateral. Lenders conduct technical and legal verification to ensure the property is worth the stated value and has clear title.

Monthly income: 1.5 lakhs Maximum EMI allowed (50%): 75,000 rupees Existing EMIs: 15,000 rupees Available for home loan EMI: 60,000 rupees

At 9 percent interest for 20 years, 60,000 rupees EMI supports a loan of approximately 54 lakhs. With 20 percent down payment, you can purchase a property worth approximately 67.5 lakhs.

Interest rate remains constant throughout the loan tenure. Provides certainty about EMI amount. Typically 0.5 to 1 percent higher than floating rates. Suitable if you expect interest rates to rise.

Interest rate varies based on the lender's benchmark rate. EMI changes when rates change. Lower initial rates compared to fixed. Suitable if you expect rates to remain stable or decline.

Fixed rate for initial 2 to 5 years, then converts to floating. Provides initial certainty with later flexibility. Rates typically between pure fixed and floating.

Most borrowers in India choose floating rate loans due to lower rates and the ability to benefit if rates decline.

Longer tenure reduces EMI but increases total interest paid. Shorter tenure increases EMI but reduces total interest cost.

| Tenure | Monthly EMI | Total Investment | Total Payment |

|---|---|---|---|

| 10 years | ₹63,340 | ₹26 lakhs | ₹76 lakhs |

| 15 years | ₹50,710 | ₹41.3 lakhs | ₹91.3 lakhs |

| 20 years | ₹45,000 | ₹58 lakhs | ₹1.08 crores |

| 25 years | ₹42,000 | ₹76 lakhs | ₹1.26 crores |

Choose tenure based on your EMI affordability and investment goals. Longer tenure makes sense if you plan to invest the EMI savings in higher return assets. Shorter tenure works if you want to own the property outright sooner.

Home loans offer significant tax benefits that reduce the effective cost of ownership and improve investment returns.

You can claim deduction up to 1.5 lakhs annually on the principal amount repaid during the financial year. This deduction is part of the overall 80C limit that includes EPF, PPF, life insurance, and other eligible investments.

The deduction is available only after you receive possession of the property. For under construction properties, you cannot claim this benefit until possession is received.

You can claim deduction on the interest paid on your home loan. The deduction limit depends on whether the property is self occupied or let out.

Maximum deduction of 2 lakhs per financial year on interest paid. This limit applies even if actual interest paid is higher. Available from the year you receive possession or the loan is sanctioned, whichever is later.

Unlimited deduction on interest paid. The entire interest amount can be claimed as deduction against rental income. If rental income is less than interest, the loss can be set off against other income up to 2 lakhs per year.

First time homebuyers purchasing property valued up to 45 lakhs can claim additional deduction of up to 1.5 lakhs on interest paid. This is over and above the 2 lakh limit under Section 24(b).

This benefit is available for loans sanctioned between April 2019 and March 2022, though extensions may be announced.

You purchase a property for 80 lakhs with a loan of 64 lakhs at 9 percent for 20 years. Your annual EMI is 6.9 lakhs, comprising approximately 5.7 lakhs interest and 1.2 lakhs principal in the first year.

If you are in the 30 percent tax bracket, these deductions save approximately 96,000 rupees in taxes annually. This reduces your effective annual cost from 6.9 lakhs to 5.94 lakhs, improving your return on investment.

If you rent out the property, you can claim unlimited interest deduction against rental income. Suppose you receive 30,000 rupees monthly rent (3.6 lakhs annually) and pay 5.7 lakhs interest in the first year.

Your rental income is 3.6 lakhs. You can claim 30 percent standard deduction (1.08 lakhs), reducing taxable rental income to 2.52 lakhs. You can then deduct the full interest of 5.7 lakhs, creating a loss of 3.18 lakhs.

This loss can be set off against your other income up to 2 lakhs, reducing your overall tax liability. The remaining loss of 1.18 lakhs can be carried forward for up to 8 years to set off against future rental income.

Calculating return on investment helps you evaluate whether a property investment meets your financial goals and compare it with alternative investment options.

Simple ROI measures the total gain as a percentage of initial investment without considering the time value of money.

ROI = (Current Value - Initial Investment) / Initial Investment × 100

Example: You purchased a property for 60 lakhs five years ago. Current value is 90 lakhs.

ROI = (90 - 60) / 60 × 100 = 50%

This represents 50 percent total return over five years, or 10 percent average annual return.

This method measures annual cash flow as a percentage of actual cash invested (down payment and closing costs).

Cash on Cash Return = Annual Cash Flow / Total Cash Invested × 100

Example:

You purchased a property for 80 lakhs with 16 lakhs down payment and 64 lakh loan. Closing costs were 4 lakhs. Total cash invested is 20 lakhs.

Annual rental income is 3.6 lakhs. Annual EMI is 6.9 lakhs. Annual cash outflow is 3.3 lakhs. After tax benefits of 96,000 rupees, net annual outflow is 2.34 lakhs.

Cash on Cash Return = -2.34 / 20 × 100 = -11.7%

The negative return indicates you are paying money out of pocket annually. However, this doesn't account for principal repayment (which builds equity) and property appreciation.

Total return includes rental income, principal repayment, property appreciation, and tax benefits.

Example:

Initial investment: 20 lakhs (down payment and costs) Annual rental income: 3.6 lakhs Annual EMI: 6.9 lakhs (5.7 lakhs interest, 1.2 lakhs principal) Annual out of pocket: 3.3 lakhs Tax benefits: 96,000 rupees Net annual cost: 2.34 lakhs

This seems low, but remember you control an asset worth 90 lakhs with only 31.7 lakhs invested, and you still own the property which will continue appreciating.

IRR considers the time value of money and provides the most accurate return calculation. It accounts for the timing of all cash flows including initial investment, monthly outflows, and final sale proceeds.

Calculating IRR requires financial calculators or Excel. For the example above, assuming you sell after 5 years for 90 lakhs and repay the 57.5 lakh loan, your net proceeds are 32.5 lakhs.

Your cash flows are:

The IRR for these cash flows is approximately 8.5 percent annually, which represents your true annualized return.

Many investors underestimate the total cost of property ownership by focusing only on the purchase price and EMI. Several hidden costs can significantly impact your returns.

Stamp duty rates vary by state, ranging from 3 to 8 percent of property value. Registration charges add another 1 percent. For an 80 lakh property in a state with 5 percent stamp duty, you pay 4 lakhs stamp duty and 80,000 rupees registration, totaling 4.8 lakhs.

Some states offer reduced stamp duty for women buyers, typically 1 to 2 percent lower than standard rates.

Properties under construction attract 5 percent GST on the construction value (after deducting land component). For practical purposes, expect GST of approximately 3 to 4 percent of total property value.

For an 80 lakh under construction property, GST could be 2.4 to 3.2 lakhs. This is included in the property price quoted by builders, but you need to account for it in your budget.

Banks charge processing fees of 0.25 to 1 percent of loan amount, typically with a minimum of 5,000 to 10,000 rupees. For a 64 lakh loan, processing fees could be 16,000 to 64,000 rupees.

Some banks waive processing fees during promotional periods. Negotiate this fee when comparing loan offers.

Hiring a lawyer to verify property documents costs 10,000 to 50,000 rupees depending on property value and complexity. Technical verification by an engineer costs 5,000 to 15,000 rupees.

While banks conduct their own verification for loan approval, independent verification protects your interests and may uncover issues the bank missed.

Municipal corporations levy annual property tax based on property value, location, and usage. Rates vary widely, from 0.05 to 0.2 percent of property value annually.

For an 80 lakh property, annual property tax could be 4,000 to 16,000 rupees. This is an ongoing cost you pay as long as you own the property.

Apartments in complexes charge monthly maintenance for upkeep of common areas, security, and amenities. Charges range from 2 to 6 rupees per square foot per month.

For a 1,000 square foot apartment, monthly maintenance could be 2,000 to 6,000 rupees or 24,000 to 72,000 rupees annually.

Budget for periodic repairs including painting, plumbing fixes, electrical work, and appliance replacement. A reasonable estimate is 0.5 to 1 percent of property value annually.

For an 80 lakh property, budget 40,000 to 80,000 rupees annually for repairs and maintenance.

Rental properties experience vacancy when tenants move out and you search for new tenants. Budget for 1 to 2 months vacancy annually, during which you receive no rent but continue paying EMI and maintenance.

Finding tenants through brokers costs 0.5 to 1 month rent. For a property renting at 30,000 rupees monthly, brokerage is 15,000 to 30,000 rupees each time you find a new tenant.

These costs significantly impact your returns and must be factored into affordability calculations and ROI projections.

Proper legal due diligence and documentation protect your investment and prevent future disputes. Understanding the legal aspects of property purchase is essential for every investor.

Before purchasing any property, verify that the seller can provide all necessary documents proving legal ownership and clear title.

Title verification confirms that the seller has legal ownership and the right to sell the property. This is the most critical step in property purchase.

Review the sale deed in the seller's name. Verify the seller's name matches exactly with the name on the deed. Check the property description including survey number, plot number, and boundaries. Confirm the deed is registered with the sub registrar office.

Obtain copies of all previous sale deeds for the past 30 years. Verify each transfer was legal and properly registered. Ensure no gaps in the ownership chain. Check for any disputes or litigation in previous transfers.

Obtained an encumbrance certificate from the sub registrar office for the past 13 to 30 years. Review all transactions listed in the certificate. Confirm no mortgages, liens, or legal claims exist. Verify all previous loans have been closed and satisfied.

Search court records for any pending litigation related to the property. Verify no cases are filed regarding ownership, partition, or other disputes. Check with local police for any criminal cases related to the property.

Obtain property tax receipts for the past 5 years. Verify the property description in tax records matches the title deed. Confirm no dues are pending with the municipal corporation.

Check the property's zoning classification with municipal authorities. Confirm the current use matches the approved land use. Verify no violations of zoning regulations exist.

Visit the property and verify it matches the description in documents. Check boundaries match the survey numbers and measurements. Confirm no encroachments exist on the property. Verify no unauthorized construction has been done.

Engage a property lawyer to review all documents. Get technical verification from an engineer or architect. Consider title insurance for additional protection.

The Real Estate (Regulation and Development) Act, 2016 provides protection to homebuyers and ensures transparency in real estate transactions. Understanding RERA compliance helps you choose legitimate projects and avoid fraud.

All residential projects with plot area exceeding 500 square meters or 8 apartments must register with the state RERA authority. Developers must provide detailed project information including land status, approvals, layout plans, and completion timeline.

Visit your state RERA website and search for the project by name or registration number. Verify the project is registered and registration is current. Review the project details and ensure they match what the developer claims. Check quarterly progress reports to assess actual construction progress. Verify the developer is depositing buyer funds in the designated escrow account.

Developers cannot advertise or sell without RERA registration. This ensures only legitimate projects with proper approvals reach the market.

70 percent of buyer payments must be deposited in a separate escrow account. These funds can only be used for that specific project. This prevents diversion of funds to other projects.

RERA defines carpet area as the net usable area within the apartment. This prevents developers from inflating area calculations. Buyers know exactly what usable space they are purchasing.

Developers must specify completion date in the agreement. Delays beyond this date attract penalties payable to buyers. Buyers can claim compensation for delayed possession.

Developers are liable for structural defects for 5 years from possession. Buyers can claim repairs for defects discovered within this period. This ensures quality construction and proper maintenance.

RERA provides a dedicated dispute resolution mechanism. Complaints are resolved faster than traditional civil courts. Buyers have recourse against developer defaults or violations.

The sale deed is the legal document that transfers property ownership from seller to buyer. Proper execution and registration of the sale deed is essential for legal ownership.

A lawyer prepares the sale deed draft based on the sale agreement. Both parties review the draft and suggest changes if needed. The final draft is agreed upon by both parties.

Calculate stamp duty based on state rates and property value. Purchase stamp paper or pay stamp duty online depending on state procedures. Obtain stamp duty payment receipt.

Book an appointment with the sub registrar office. Both seller and buyer must be present with original documents. Bring two witnesses with valid ID proof.

Submit the sale deed along with supporting documents. Pay registration fees (typically 1 percent of property value). The sub registrar verifies documents and identities.

Both parties provide biometric fingerprints and photographs. This prevents future disputes about identity and signatures.

The sub registrar registers the deed in official records. Both parties receive a copy of the registered sale deed. The registration number and date are noted on the deed.

Update property tax records with the municipal corporation. Transfer utility connections to your name. Inform the housing society (for apartments) about the ownership change.

Several common legal issues can create problems for property buyers. Awareness and proper due diligence help avoid these pitfalls.

Never purchase property without thorough title verification. Unclear title can result in ownership disputes, inability to sell in future, or even loss of the property. Always hire a lawyer to verify title and obtain title insurance if available.

Properties with existing mortgages, liens, or legal claims create complications. Ensure the seller clears all encumbrances before purchase. Obtain an updated encumbrance certificate just before registration.

Documents may be in order, but the physical property may have issues. Always visit the property and verify boundaries, construction quality, and absence of encroachments. Check for unauthorized construction or zoning violations.

Developers often make verbal promises about amenities, specifications, or timelines. Ensure all promises are documented in the sale agreement. Verbal promises have no legal value and cannot be enforced.

Many buyers sign agreements without reading them carefully. The agreement contains important terms about payment schedule, possession date, penalties, and dispute resolution. Read every clause and seek clarification for anything unclear.

Always demand official receipts for all payments made to the developer. Payments without receipts cannot be proven and may be denied by the developer. Ensure receipts mention your name, property details, and amount paid.

Buying from unregistered projects carries significant risk. The developer may not have proper approvals or may divert your funds. Always verify RERA registration before making any payment.

Some buyers delay sale deed registration to save stamp duty or for other reasons. Unregistered sale deeds have no legal validity. You do not legally own the property until the deed is registered. Register the deed immediately after purchase.

Real estate investment carries various risks that can impact returns or result in capital loss. Understanding these risks and implementing mitigation strategies protects your investment.

Market risk refers to the possibility that property values may decline due to economic conditions, oversupply, or changing demand patterns.

Economic recessions reduce employment, income, and buyer confidence. Property demand falls, leading to price corrections and longer selling times. Rental demand may also decline as people double up or move to cheaper accommodations.

Excessive construction in an area can create oversupply, leading to price stagnation or decline. Rental yields also suffer as landlords compete for limited tenants.

Rising interest rates increase EMI for floating rate loans. Higher rates also reduce affordability for new buyers, potentially dampening demand and prices.

Choose fixed rate loans if you expect rates to rise Keep EMI well below maximum affordability to absorb rate increases Make prepayments when possible to reduce principal and interest burden Monitor rate trends and consider refinancing if better rates become available

Real estate is an illiquid asset that can take months or years to sell. During market downturns, liquidity worsens as buyer demand falls.

The developer's reputation, financial strength, and track record significantly impact project completion and quality. Buying from unreliable developers can result in delays, poor construction, or project abandonment.

Research the developer's history and past projects. How many projects have they completed? Were projects delivered on time? Visit completed projects and speak with residents about their experience. Check online reviews and ratings on property portals.

Review the developer's financial statements if they are a listed company. Check their debt levels and cash flow. Developers with high debt may struggle to complete projects. Verify they have funding arrangements for the project.

Check if the developer has registered all projects with RERA. Review quarterly progress reports for timely updates. Developers who comply with RERA are more likely to be reliable.

Search for any legal cases against the developer. Check with consumer forums for complaints. Developers with numerous legal disputes may have quality or delivery issues.

Verify the developer has obtained all necessary approvals. Check for building plan approval, environmental clearances, and NOCs. Developers who start construction without approvals face project delays.

Be cautious of developers demanding large upfront payments. RERA mandates construction linked payment plans. Developers asking for full payment before completion may have cash flow issues.

Location determines property appreciation, rental demand, and quality of life. Poor location choices can result in stagnant values and difficulty finding tenants or buyers.

How easily can you reach employment hubs, schools, hospitals, and shopping areas? Are there multiple route options or just one congested road? What is the impact of upcoming metro or highway projects?

What is the quality of roads, water supply, electricity, and sewage systems? Are there frequent power cuts or water shortages? Is the area prone to flooding during monsoons?

Are there good schools within reasonable distance? What hospitals are available for medical emergencies? Are there parks, shopping centers, and entertainment options?

What is the crime rate in the area? Is the neighborhood well lit at night? Are there police stations and emergency services nearby?

What infrastructure projects are planned for the area? Are there upcoming commercial or IT developments that will drive demand? Could negative developments like industrial projects impact livability?

Is the area prone to pollution from industries or traffic? Are there green spaces and parks? Is the area near airports with noise pollution?

What is the profile of residents in the area? Are properties well maintained? Is there a sense of community? Are there issues with illegal construction or encroachments?

Insurance products provide financial protection against various risks associated with property ownership.

Home insurance covers the structure and contents against damage from fire, natural disasters, theft, and other perils.

Annual premium ranges from 0.1 to 0.5 percent of property value depending on coverage and location. For an 80 lakh property, annual premium is 8,000 to 40,000 rupees.

Title insurance protects against financial loss from defects in property title. This is a new product in India with limited availability.

One time premium of 0.1 to 0.5 percent of property value. For an 80 lakh property, premium is 8,000 to 40,000 rupees for lifetime coverage.

This insurance pays your home loan EMI if you lose your job or become disabled.

Annual premium of 0.5 to 1.5 percent of outstanding loan amount. For a 60 lakh loan, annual premium is 30,000 to 90,000 rupees.

While not specific to property, term insurance ensures your family can repay the home loan if you die.

Choose term insurance coverage at least equal to your outstanding home loan. This ensures your family inherits the property without debt burden.

Term insurance is inexpensive, with an annual premium of 10,000 to 30,000 rupees for 1 crore coverage for a 35 year old.

Planning your exit strategy before investing helps you maximize returns and avoid forced sales at unfavorable prices.

Timing your property sale impacts the returns you realize. Several factors should influence your selling decision.

If the property has appreciated to your target return level, consider selling even if market conditions suggest further appreciation is possible. Locking in gains is better than waiting for perfect timing that may never come.

Rapid price increases of 15 to 20 percent annually, excessive new construction, easy credit availability, and speculative buying suggest market peaks. Selling near peaks maximizes returns, though timing peaks perfectly is difficult.

Life events like children's education, medical emergencies, or business opportunities may require capital. Selling property to meet genuine needs makes sense even if market timing is not optimal.

If you identify investments with better risk adjusted returns, selling property to redeploy capital can improve overall portfolio returns.

Properties held for more than 24 months qualify for long term capital gains tax at 20 percent with indexation benefits. Selling before 24 months attracts short term capital gains tax at 30 percent plus surcharge. The tax difference often justifies holding for at least 24 months.

Real estate markets move in cycles of 5 to 8 years. Selling during the growth phase of the cycle maximizes returns. Avoid selling during downturns unless absolutely necessary.

Several strategies can help you achieve the best possible price when selling your property.

Regular maintenance preserves property value and appeals to buyers. Fresh paint, working fixtures, and clean common areas create positive impressions. Address any structural issues or leaks promptly.

List your property during peak buying seasons, typically January to March and August to October. Avoid listing during festivals or summer months when buyer activity slows.

Research comparable property sales in your area. Price within 5 to 10 percent of market rates. Overpricing leads to extended selling times and eventual price reductions that signal desperation.

Quality photos in listings attract more buyer inquiries. Hire a professional photographer or use good equipment and lighting. Show the property in its best condition.

Present the property clean, decluttered, and well lit. Remove personal items and excess furniture. Create a neutral environment that allows buyers to envision themselves living there.

Accommodate buyer viewing requests, including evenings and weekends. The more buyers who view the property, the higher the chance of receiving good offers.

Emphasize aspects that differentiate your property like park facing, corner unit, recent renovation, or proximity to metro. These features justify premium pricing.

Have all documents ready including title deed, tax receipts, society NOC, and occupancy certificate. Buyers appreciate transparency and are willing to pay more for hassle free transactions.

Small investments in new fixtures, fresh paint, or modern lighting can significantly improve perceived value. Spend 1 to 2 percent of property value on upgrades that can increase sale price by 3 to 5 percent.

Selling property triggers capital gains tax that reduces your net proceeds. Understanding tax implications helps you plan exits efficiently.

Properties sold within 24 months of purchase attract short term capital gains tax. The gain is calculated as sale price minus purchase price and improvement costs. This gain is added to your income and taxed at your applicable income tax slab rate of 30 percent plus surcharge and cess.

Purchase price: 60 lakhs Sale price after 18 months: 72 lakhs Capital gain: 12 lakhs Tax at 30% plus cess: 3.74 lakhs Net proceeds: 68.26 lakhs

Properties sold after 24 months attract long term capital gains tax at 20 percent plus surcharge and cess. You can claim an indexation benefit, which adjusts the purchase price for inflation using the Cost Inflation Index published by the government.

Purchase price in 2021: 60 lakhs Sale price in 2026: 90 lakhs Cost Inflation Index 2021: 317 Cost Inflation Index 2026: 363 (assumed) Indexed purchase price: 60 × (363/317) = 68.7 lakhs Capital gain: 90 - 68.7 = 21.3 lakhs Tax at 20% plus cess: 5.59 lakhs Net proceeds: 84.41 lakhs

If you invest the capital gains in another residential property within specified timelines, you can claim exemption from capital gains tax. You must purchase the new property within 1 year before or 2 years after the sale, or construct within 3 years after the sale.

The new property must be residential and you cannot sell it for 3 years. If you invest only part of the gains, proportionate exemption is available.

You can invest capital gains in specified bonds (currently NHAI and REC bonds) within 6 months of sale. Maximum investment allowed is 50 lakhs. The bonds have a 5 year lock in period. Interest earned is taxable.

If you sell any asset other than a residential house and invest proceeds in a residential property, you can claim exemption. This section is useful for selling commercial property, land, or other assets.

When you need to exit a property investment, you can either sell or continue renting. The decision depends on multiple factors.

| Factor | Sell | Rent |

|---|---|---|

| Need capital now | Yes | No |

| High appreciation expected | No | Yes |

| Good rental yield | No | Yes |

| Market at peak | Yes | No |

| High capital gains tax | No | Yes |

| Property needs major repair | Yes | No |

| Want passive income | No | Yes |

| Simplify portfolio | Yes | No |

Some investors use a hybrid approach, selling a portion of their property portfolio while retaining properties with the best fundamentals. This provides capital for current needs while maintaining exposure to real estate appreciation and rental income.

Various tools and platforms help investors make informed decisions, calculate returns, and execute transactions efficiently.

Online calculators simplify complex financial calculations and help you evaluate investment scenarios.

Calculates monthly EMI based on loan amount, interest rate, and tenure. Helps you determine affordability and compare different loan options. Shows the split between principal and interest components.

Estimates the loan amount you qualify for based on your income, age, and existing obligations. Helps you determine the property price range you can afford.

Calculates gross and net rental yield based on property value, rental income, and expenses. Helps you compare rental returns across different properties.

Computes short term or long term capital gains tax based on purchase price, sale price, holding period, and indexation. Helps you plan tax efficient exits.

Calculates return on investment considering purchase price, appreciation, rental income, and costs. Provides total return and annualized return percentages.

Estimates stamp duty and registration charges based on property value and state. Helps you budget for transaction costs.

Several platforms provide property listings, price trends, and market intelligence.

Websites like MagicBricks, 99acres, Housing.com, and NoBroker list properties for sale and rent. They provide price trends, locality reviews, and builder information. Use these to research market rates and compare properties.

Each state has a RERA website with registered project details. Use these to verify project registration, check developer compliance, and review project progress reports.

Websites like igrs.gov.in provide property registration information. Municipal corporation websites offer property tax details and approved building plans.

PropTiger, Square Yards, and Anarock provide market research reports, price indices, and investment analysis. These help you understand market trends and identify investment opportunities.

TogetherBuying has emerged as a leading platform for group property buying, offering several advantages to investors.

Traditional property purchases involve brokerage of 1 to 2 percent paid by the buyer. TogetherBuying eliminates this cost, saving 1 to 2 lakhs on a 1 crore property.

The platform brings together multiple buyers to negotiate bulk purchase discounts from builders. Discounts typically range from 5 to 12 percent below market rates, translating to savings of 5 to 12 lakhs on a 1 crore property.

TogetherBuying conducts due diligence on all listed projects, verifying RERA registration, legal clearances, and builder credentials. This reduces the risk of dealing with fraudulent developers or projects with legal issues.

All negotiations, pricing, and terms are documented and shared with group members. This transparency ensures everyone receives the same benefits and prevents hidden charges.

Beyond price discounts, the platform often negotiates additional benefits like free car parking, club membership, or upgraded specifications. These add value without increasing the purchase price.

TogetherBuying assists with home loan processing, legal documentation, and property registration. This support simplifies the purchase process, especially for first time buyers.

The platform connects investors interested in similar projects or locations. This community provides knowledge sharing, market insights, and networking opportunities.

The platform identifies upcoming or ongoing projects from reputable builders. It creates a group of interested buyers for each project. The group collectively approaches the builder to negotiate better terms. Once terms are finalized, each member completes their individual purchase with the negotiated benefits.

A group of 20 investors used TogetherBuying to purchase apartments in a Bangalore project. The builder's listed price was 95 lakhs for 2 BHK units. Through group negotiation, the price was reduced to 87 lakhs, a discount of 8 lakhs or 8.4 percent. Additionally, the group received free covered parking worth 3 lakhs and club membership worth 2 lakhs. Total benefits per investor were 13 lakhs or 13.7 percent of the original price.

Another group in Pune negotiated a 10 percent discount plus upgraded flooring and fixtures worth 4 lakhs. The total savings of 14 lakhs on a 1 crore property significantly improved the investment returns.

Professional legal advice protects your investment and ensures compliance with regulations.

Property lawyer fees vary based on property value and complexity. For straightforward transactions, expect to pay 10,000 to 30,000 rupees. For complex cases involving title disputes or litigation, fees can range from 50,000 to 2 lakhs or more.

Many lawyers charge a percentage of property value, typically 0.5 to 1 percent. For a 1 crore property, legal fees would be 50,000 to 1 lakh.

Real estate investment in India offers significant wealth creation potential when approached with proper knowledge, planning, and execution. The 2026 market presents opportunities across multiple cities and property types, driven by urbanization, infrastructure development, and economic growth.

Success in real estate investment requires understanding market dynamics, choosing the right strategy aligned with your goals, conducting thorough due diligence, planning finances carefully, and managing risks effectively. The tools, platforms, and resources available today make property investment more accessible and transparent than ever before.

Whether you choose to invest in physical properties for long term appreciation, rental properties for passive income, or REITs for liquidity and diversification, the key is to start with clear objectives, invest within your means, and maintain a long term perspective. Real estate rewards patient investors who focus on fundamentals rather than chasing short term speculation.

Platforms like TogetherBuying are democratizing access to better deals and making group buying a viable strategy for individual investors. The regulatory improvements through RERA provide better protection and transparency. The expanding range of financing options makes property ownership achievable for more Indians.

As you embark on your real estate investment journey, remember that knowledge is your most valuable asset. Continue learning about markets, regulations, and strategies. Seek professional advice when needed. Start small if necessary, but start. The best time to invest in real estate was yesterday. The second best time is today.

Contact Us

Fill out this form

& we'll get back

to you

Recommended for you