Market Trends

How to Calculate ROI on Real Estate Investment?

24 Dec 2025

Market Trends

24 Dec 2025

Content

No Blogs content found

It looks like there haven’t been any blogs yet!

Calculating return on investment (ROI) is the most critical skill for real estate investors. Without accurate ROI calculations, you cannot evaluate whether a property meets your financial goals or compare different investment opportunities effectively.

A 2024 study by ANAROCK Property Consultants found that 58 percent of first time property investors in India do not calculate ROI before purchasing, relying instead on gut feeling or broker recommendations. This lack of financial analysis often leads to disappointing returns and missed opportunities.

This comprehensive guide teaches you five essential ROI calculation methods with real world examples from Indian property markets. Whether you are evaluating a 50 lakh apartment in Pune or a 1.5 crore commercial space in Bangalore, these formulas help you make data driven investment decisions.

ROI calculation serves multiple critical purposes in your investment journey.

Compare Investment Options: ROI allows you to compare a property investment against stocks, mutual funds, fixed deposits, or other real estate opportunities on an apples to apples basis.

Set Realistic Expectations: Understanding potential returns helps you avoid overpaying for properties or expecting unrealistic appreciation that never materializes.

Identify Value Opportunities: Properties with higher ROI relative to market averages represent better value, even if absolute prices seem high.

Plan Cash Flow: ROI calculations reveal whether rental income covers your EMI and expenses, or if you need to contribute from your pocket monthly.

Time Your Exit: Knowing your current returns helps you decide when to sell and redeploy capital to higher yielding opportunities.

Simple ROI measures total gain as a percentage of initial investment. This basic formula provides a quick snapshot of investment performance.

You purchased a 2 BHK apartment in Pune five years ago for the following costs:

Total gain = 75 lakhs - 54.5 lakhs = 20.5 lakhs Simple ROI = 20.5 ÷ 54.5 × 100 = 37.6% This represents 37.6 percent total return over 5 years, or approximately 7.5 percent average annual return.

This method does not account for rental income received during the holding period, ongoing expenses like maintenance and property tax, loan interest paid if you used financing, or the time value of money. Despite these limitations, simple ROI provides a quick way to assess capital appreciation, which is useful for preliminary property evaluation.

Rental yield measures annual rental income as a percentage of property value. This metric indicates the cash flow generation capacity of your investment.

Gross Rental Yield Formula: Annual Rent ÷ Property Value × 100 Net Rental Yield Formula: (Annual Rent - Annual Expenses) ÷ Property Value × 100

You own a 3 BHK apartment in Bangalore with the following details:

Gross yield = 3.36 ÷ 80 × 100 = 4.2%

Net annual income = 3.36 lakhs - 0.6 lakhs = 2.76 lakhs Net yield = 2.76 ÷ 80 × 100 = 3.45%

| City | Typical Gross Yield | Typical Net Yield | Market Status |

|---|---|---|---|

| Mumbai | 2–2.5% | 1.5–2% | Low yield, high appreciation |

| Bangalore | 2.5–3.5% | 2–3% | Moderate yield, high growth |

| Hyderabad | 3–4% | 2.5–3.5% | Good yield, strong growth |

| Pune | 2.5–3% | 2–2.5% | Moderate yield, steady growth |

| Ahmedabad | 3–3.5% | 2.5–3% | Good yield, emerging market |

| Gurgaon | 2–3% | 1.5–2.5% | Moderate yield, stable market |

This metric is most useful for comparing rental income potential across different properties or cities. Investors focused on cash flow prioritize properties with yields above 3 percent, while those seeking appreciation may accept lower yields in high growth areas.

Cash on cash return measures annual cash flow as a percentage of actual cash invested (down payment and closing costs). This metric is crucial for leveraged investments using home loans.

You purchase a property for 70 lakhs with the following structure:

Annual rental income: 3.6 lakhs Less: Annual expenses: 0.76 lakhs Less: Annual EMI: 6.05 lakhs Annual cash outflow: 3.21 lakhs

Cash outflow: 3.21 lakhs Less: Tax savings: 0.96 lakhs Net cash outflow: 2.25 lakhs

Return = -2.25 ÷ 20 × 100 = -11.25%

The negative return indicates you are paying money out of pocket annually. However, this does not account for equity building through principal repayment and property appreciation.

If you account for principal repayment as equity building:

Principal repaid in year 1: 1.2 lakhs Net cash outflow: 2.25 lakhs Actual cost after equity building: 1.05 lakhs

Adjusted return = -1.05 ÷ 20 × 100 = -5.25%

This metric improves each year as rent increases and loan principal repayment accelerates.

![]()

Total return combines all income sources (rental income, principal repayment, property appreciation, tax benefits) against total investment to show complete investment performance.

You purchased a property 5 years ago with the following details:

Total gain = 55 lakhs (current equity) - 28 lakhs (total investment) = 27 lakhs Total return = 27 ÷ 28 × 100 = 96.4% This represents 96.4 percent total return over 5 years, or approximately 19.3 percent annualized return.

| Component | Amount | Contribution to Return |

|---|---|---|

| Property appreciation | ₹30 lakhs | 107% |

| Principal repaid | ₹10 lakhs | 36% |

| Rental income received | ₹18 lakhs | 64% |

| Total value created | ₹55 lakhs | 207% |

| Less: Interest paid | ₹26 lakhs | −93% |

| Less: Expenses | ₹5 lakhs | −18% |

| Net gain | ₹27 lakhs | 96% |

This breakdown shows that appreciation and principal repayment drive most of the return, while interest paid is the largest cost.

IRR represents the most sophisticated ROI calculation, accounting for the time value of money and the timing of all cash flows. This metric provides the true annualized return on your investment.

IRR calculates the discount rate at which the net present value of all cash flows (initial investment, monthly outflows, final sale proceeds) equals zero. In simple terms, it shows your actual annualized return considering when money was invested or received.

You purchase a property and hold it for 7 years with the following cash flows:

Initial investment: -20 lakhs

Year 1: Net outflow -2 lakhs Year 2: Net outflow -1.8 lakhs Year 3: Net outflow -1.5 lakhs Year 4: Net outflow -1.2 lakhs Year 5: Net outflow -0.8 lakhs Year 6: Net inflow +0.5 lakhs (rent exceeds EMI) Year 7: Net inflow +1 lakh

Sale price: 1.2 crores Loan repayment: 40 lakhs Net proceeds: 80 lakhs

| Year | Cash Flow | Description |

|---|---|---|

| 0 | −₹20 lakhs | Initial investment |

| 1 | −₹2 lakhs | Net outflow |

| 2 | −₹1.8 lakhs | Net outflow |

| 3 | −₹1.5 lakhs | Net outflow |

| 4 | −₹1.2 lakhs | Net outflow |

| 5 | −₹0.8 lakhs | Net outflow |

| 6 | +₹0.5 lakhs | Net inflow |

| 7 | +₹81 lakhs | Sale proceeds + year 7 income |

Using Excel IRR function or financial calculator: IRR = 18.7% per annum

This means your investment generated an annualized return of 18.7 percent, accounting for the timing of all cash flows.

Total investment: 20 lakhs + 7.3 lakhs (net outflows) = 27.3 lakhs Final proceeds: 81 lakhs Simple return: (81 - 27.3) ÷ 27.3 = 196% over 7 years = 28% average annual

The IRR of 18.7 percent is lower than the simple average of 28 percent because it accounts for the time value of money. Money invested early in the period has more time to compound, so the true annualized return is lower than the simple average.

Each ROI calculation method serves different purposes and provides unique insights.

| ROI Method | Best Used For | Advantages | Limitations |

|---|---|---|---|

| Simple ROI | Quick property comparison | Easy to calculate | Ignores cash flow and timing |

| Rental Yield | Income property evaluation | Shows cash generation | Ignores appreciation |

| Cash on Cash | Leverage investment analysis | Measures actual cash return | Ignores equity building |

| Total Return | Complete performance assessment | Includes all value sources | Complex to calculate |

| IRR | Sophisticated analysis | Accounts for time value | Requires financial tools |

For initial property screening, use rental yield and simple ROI to quickly eliminate poor performers. For detailed analysis of shortlisted properties, calculate total return and IRR to understand true performance.

When comparing leveraged investments, cash on cash return shows how efficiently your actual cash is working. When evaluating completed investments, IRR provides the most accurate performance measure.

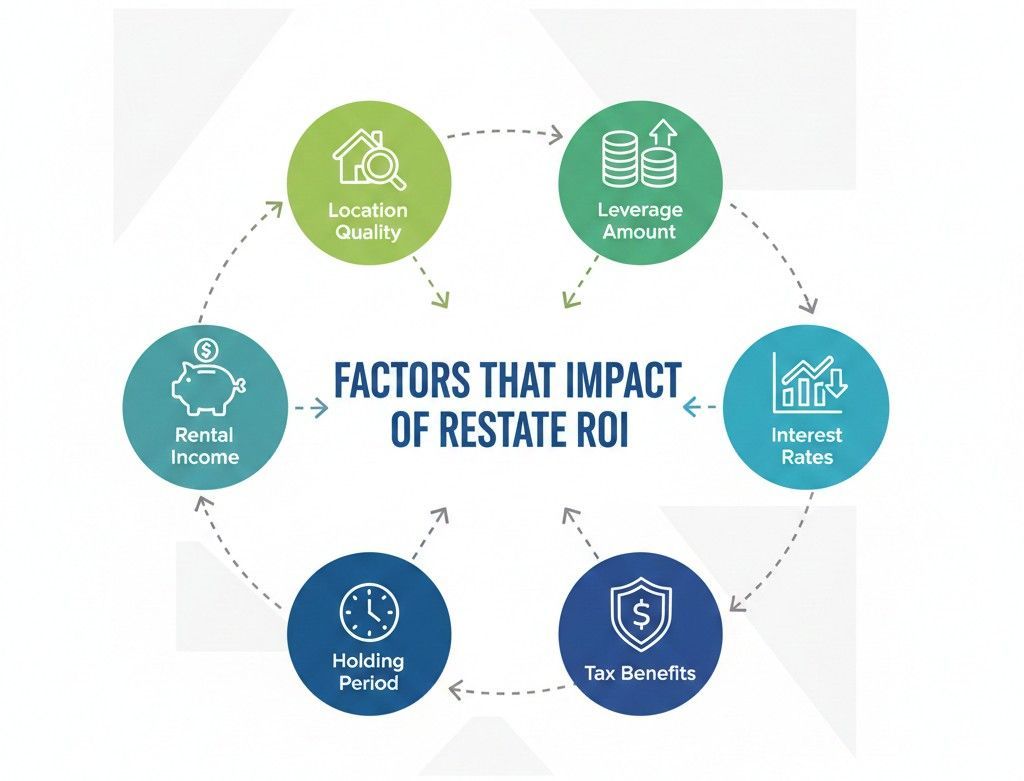

Understanding what drives ROI helps you select properties with better return potential.

Properties in areas with strong job growth, infrastructure development, and limited supply deliver higher appreciation. A property in an emerging IT corridor may appreciate 12 to 15 percent annually compared to 5 to 7 percent in established areas.

Higher leverage (larger loans) amplifies returns when property appreciates but also increases risk. A property appreciating 10 percent annually delivers 50 percent return on equity with 80 percent leverage but only 10 percent return with no leverage.

Higher rental yields reduce out of pocket costs and improve cash flow. A property yielding 4 percent requires less monthly contribution than one yielding 2 percent, improving cash on cash return.

Lower interest rates reduce EMI and improve cash flow. A 1 percent reduction in interest rate on a 50 lakh loan saves approximately 4,000 rupees monthly or 48,000 rupees annually.

Longer holding periods allow appreciation to compound and loan principal to be repaid. Properties held 10 years typically deliver better IRR than those sold after 3 to 5 years.

Maximizing deductions under Section 80C and 24(b) reduces effective costs. Tax savings of 1 lakh annually over 10 years add 10 lakhs to your returns.

Avoid these errors that lead to inaccurate return projections.

Stamp duty, registration, and legal fees add 7 to 10 percent to purchase price. Forgetting these costs inflates your ROI calculation.

Maintenance, property tax, repairs, and vacancy periods reduce net income. Failing to account for these expenses overstates rental yield.

Brokerage (1 to 2 percent) and capital gains tax (20 percent on gains) reduce net proceeds when you sell. Include these in total return calculations.

Assuming 15 to 20 percent annual appreciation based on recent hot markets leads to disappointment. Use conservative 6 to 9 percent estimates for realistic projections.

Nominal returns of 12 percent with 6 percent inflation deliver only 6 percent real returns. Consider inflation when comparing real estate to other investments.

Money invested in real estate cannot be invested elsewhere. Compare real estate ROI against returns from stocks, mutual funds, or business investments.

ROI calculations guide multiple investment decisions throughout your real estate journey.

Calculate ROI for multiple properties and choose those offering the best risk adjusted returns. A property with 14 percent IRR in a stable location may be better than one with 18 percent IRR in a risky area.

Understanding required ROI helps you determine the maximum price you should pay. If you need 15 percent IRR and a property only delivers 10 percent at asking price, negotiate a 10 to 15 percent discount.

Calculate your current ROI and compare it to alternative investments. If your property now delivers 6 percent annual return while stocks offer 12 percent, consider selling and redeploying capital.

Properties with low ROI relative to your portfolio average may be candidates for sale. Redeploy proceeds to higher yielding properties or other asset classes.

Understanding typical returns helps you evaluate whether a property offers good value.

Properties delivering returns above these benchmarks represent good value, while those below may be overpriced or in weak locations.

Several tools simplify complex ROI calculations.

Create custom spreadsheets with formulas for rental yield, cash on cash return, and IRR. Excel's IRR function calculates internal rate of return automatically from cash flow data.

Real estate investment apps like Property Calculator and Real Estate ROI provide on the go calculations during property viewings.

Property consultants and financial advisors can perform detailed ROI analysis considering tax implications, inflation, and opportunity costs.

ROI calculation is not optional for serious real estate investors. The time spent analyzing returns before purchase prevents costly mistakes and identifies opportunities others miss.

Master these calculation methods and apply them consistently to every property you evaluate. The discipline of data driven decision making separates successful real estate investors from those who rely on hope and speculation. Your financial future depends on the quality of your investment analysis, and ROI calculation forms the foundation of that analysis.

Contact Us

Fill out this form

& we'll get back

to you

Recommended for you